"Dedicated to providing clarity in complex legal environments."

Read My InsightsOtong Michael Favour is a dedicated legal and tax proffesional specializing in Alternative Disbute Resolution(ADR) and taxation, with a strong commitment to delivering practical innovative solutions at the intersection of law and finance. An Associate of the Chattered Institute of rbitrators (CIArb), trained by CIArb Kenya through the Uganda Chapter, he brings solid expertise in arbitration, mediation, and negociation, enabling the efficient and equitable resolution of disputes.

His taxation practice was shapped through experience at Godena Associates, one of Uganda's leading tax-specialized law firms, where he gained hands-on experience in tax advisory, compliance, and dispute resolution. He is well-versed in Uganda's tax framework, including the Tax procedures Code Act, and Practical exposure to regional tax jurisprudence.

Currently, Otong is Pursuing a Master of Business administration (MBA) with a focus of Finance and Taxtion, strengthening his understanding of financial strategy, tax planning and optimization. He is also undertaking a Diploma in Tax and Revenue Adminstration (DITRA) at East African School of Taxation, further enhancing his competence in tax policy, revenue mnagement and regulatory compliance.

Driven by excellence, collaboration and innovation, Otong is passionate about delivering impactful results whether resolving complex tax disputes or facilitating ambicable settlements through ADR. He welcomes opportunities in arbitration, tax advisory, and financial strategy, and is eager to connect with proffessionals across law, finance and ADR in Africa and beyond to explore meaningful collaboration and effective solutions.

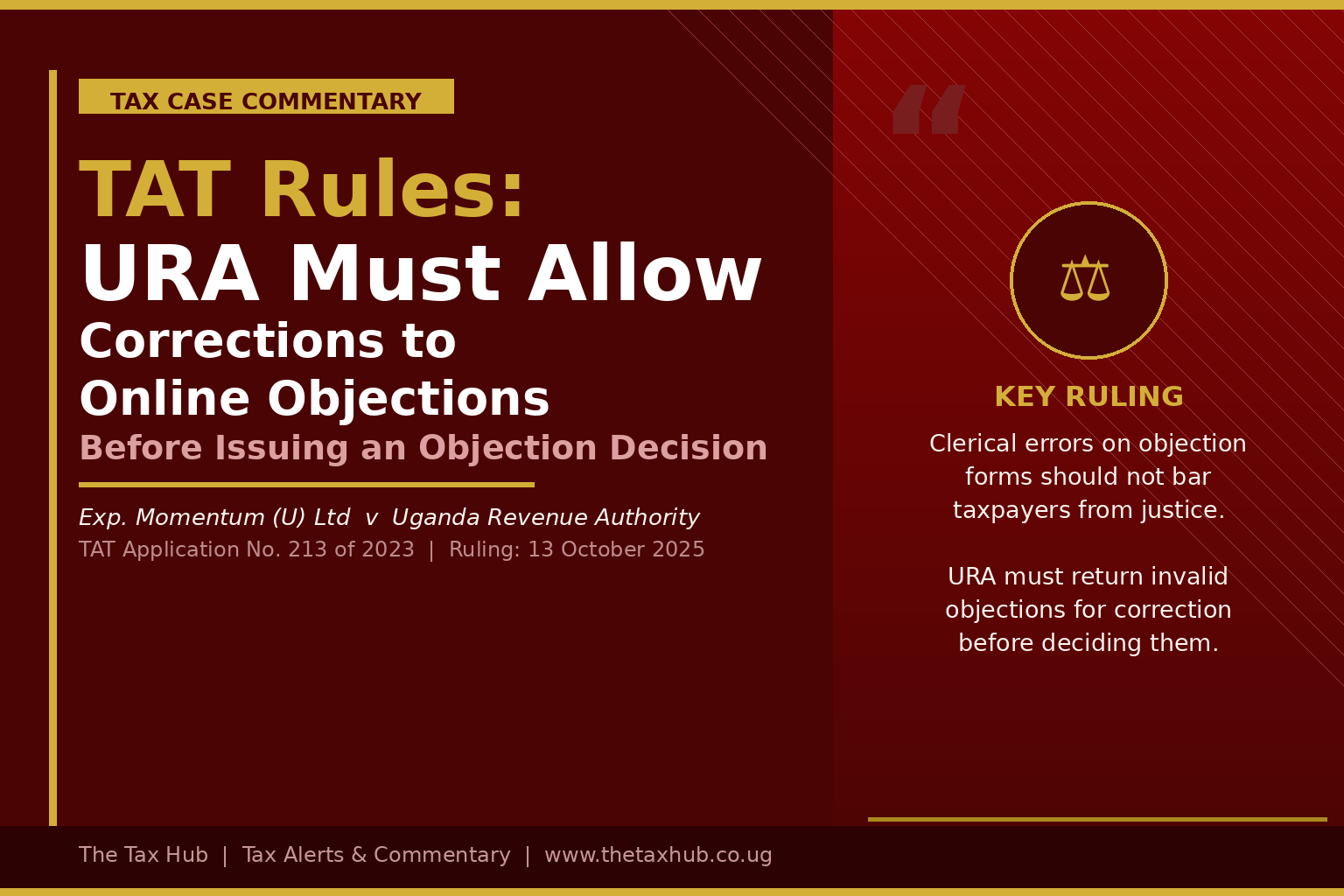

TAX CASE COMMENTARY When a Clerical Error Almost Cost a Taxpayer Everything Exp. Momentum (U) Ltd v Uganda Revenue Authority TAT Application No. 213 of 2023 | Ruling: 13th October 2025 A marketing and advertising company did everything right. It kept proper books. It reconciled its VAT and income tax returns. It gathered documents, wrote […]

Read Full Article →

Introduction Arbitration has emerged as the preferred mechanism for resolving commercial and investment disputes across the globe. At its heart lies a concept that is both deceptively simple and legally profound the seat of arbitration. The seat is not merely a pin on a map. It is the juridical home of the arbitration: a legal […]

Read Full Article →

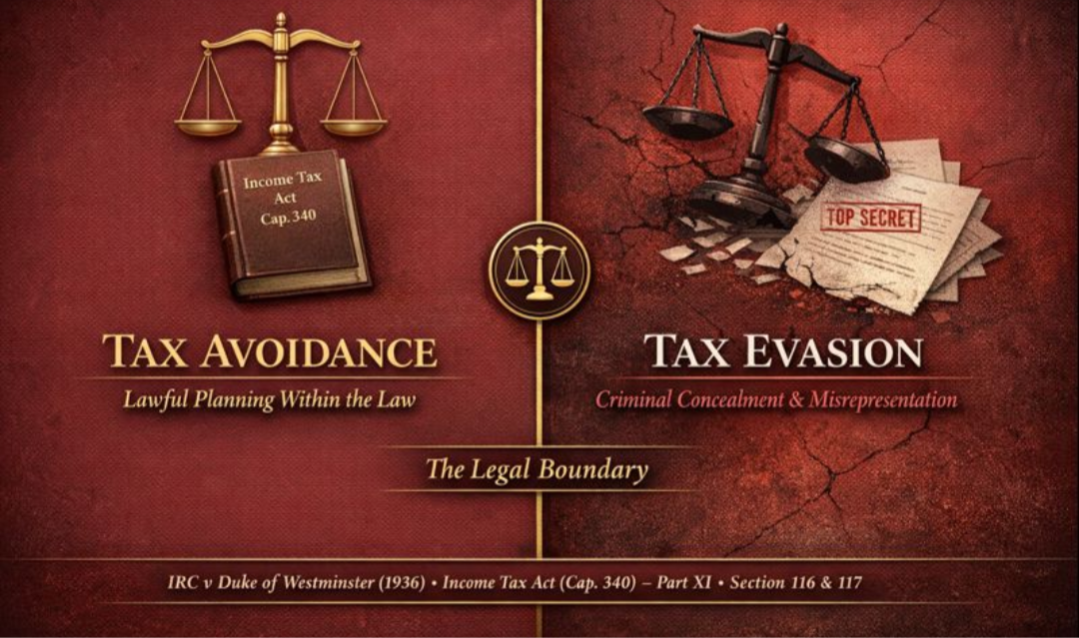

Introduction The distinction between tax avoidance and tax evasion is one of the most significant concepts in revenue law. While both practices result in a reduction of the tax payable to the state, they differ fundamentally in their legal character: one is permissible, the other is a criminal offence. This paper examines both concepts within […]

Read Full Article →

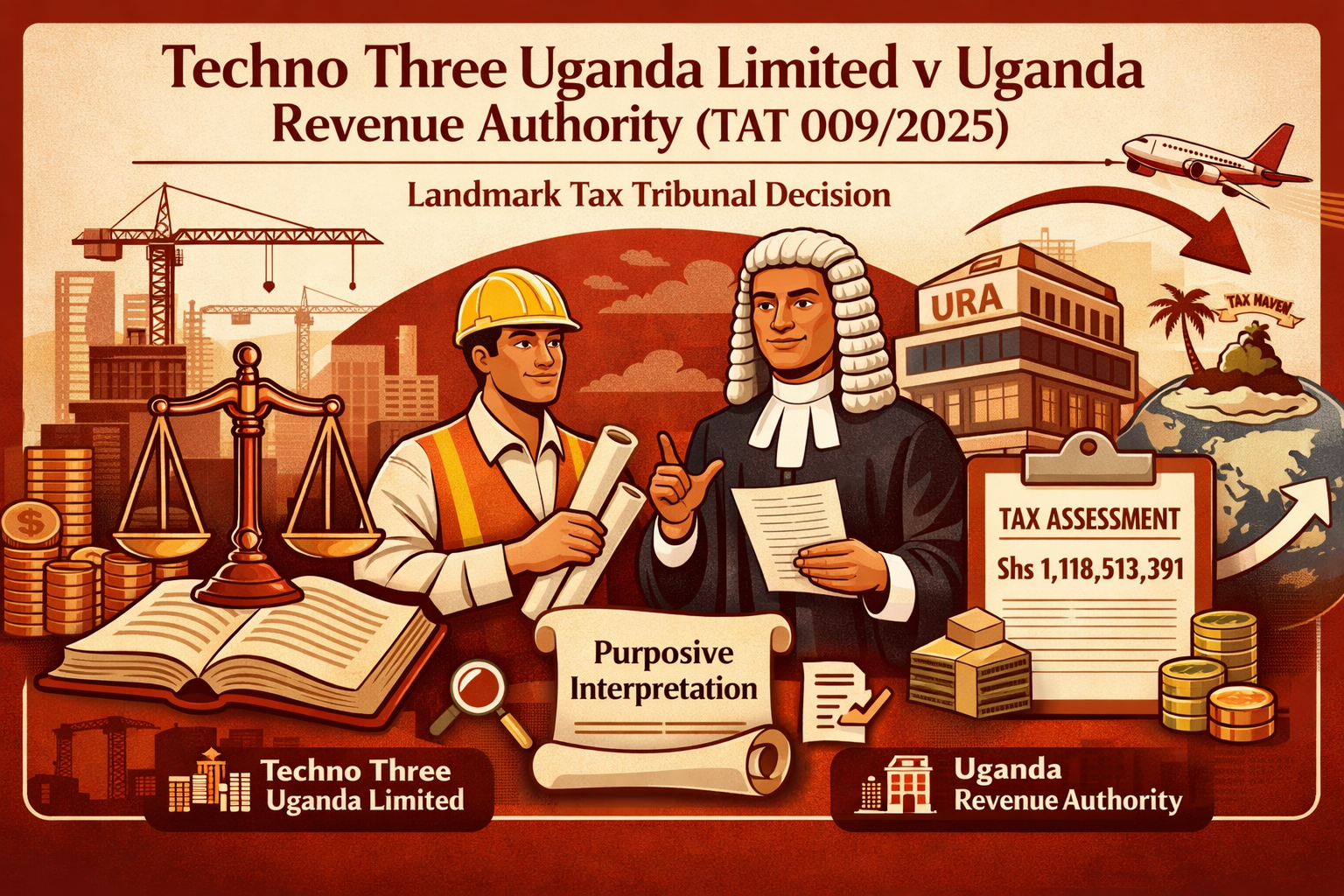

Techno Three Uganda Limited v Uganda Revenue Authority (TAT 009/2025) Introduction The Tax Appeals Tribunal’s ruling in Techno Three Uganda Limited v Uganda Revenue Authority (TAT 009/2025), delivered on 4th February 2026, represents a watershed moment in Ugandan tax jurisprudence. This case demonstrates exemplary judicial practice by applying purposive statutory interpretation to prevent absurd outcomes […]

Read Full Article →

ASIIMWE T/A ASSY LODGES V UGANDA REVENUE AUTHORITY (MISCELLANEOUS CAUSE 21 of 2025) [2025] UGTAT 3 (21 March 2025) Brief facts Assy Lodges was issued an additional income tax assessment of UGX 26,868,000 by the Uganda Revenue Authority on 11 October 2023, despite having previously declared and paid UGX 276,000 for the 2021/2022 financial year. After attempting Alternative Dispute […]

Read Full Article →