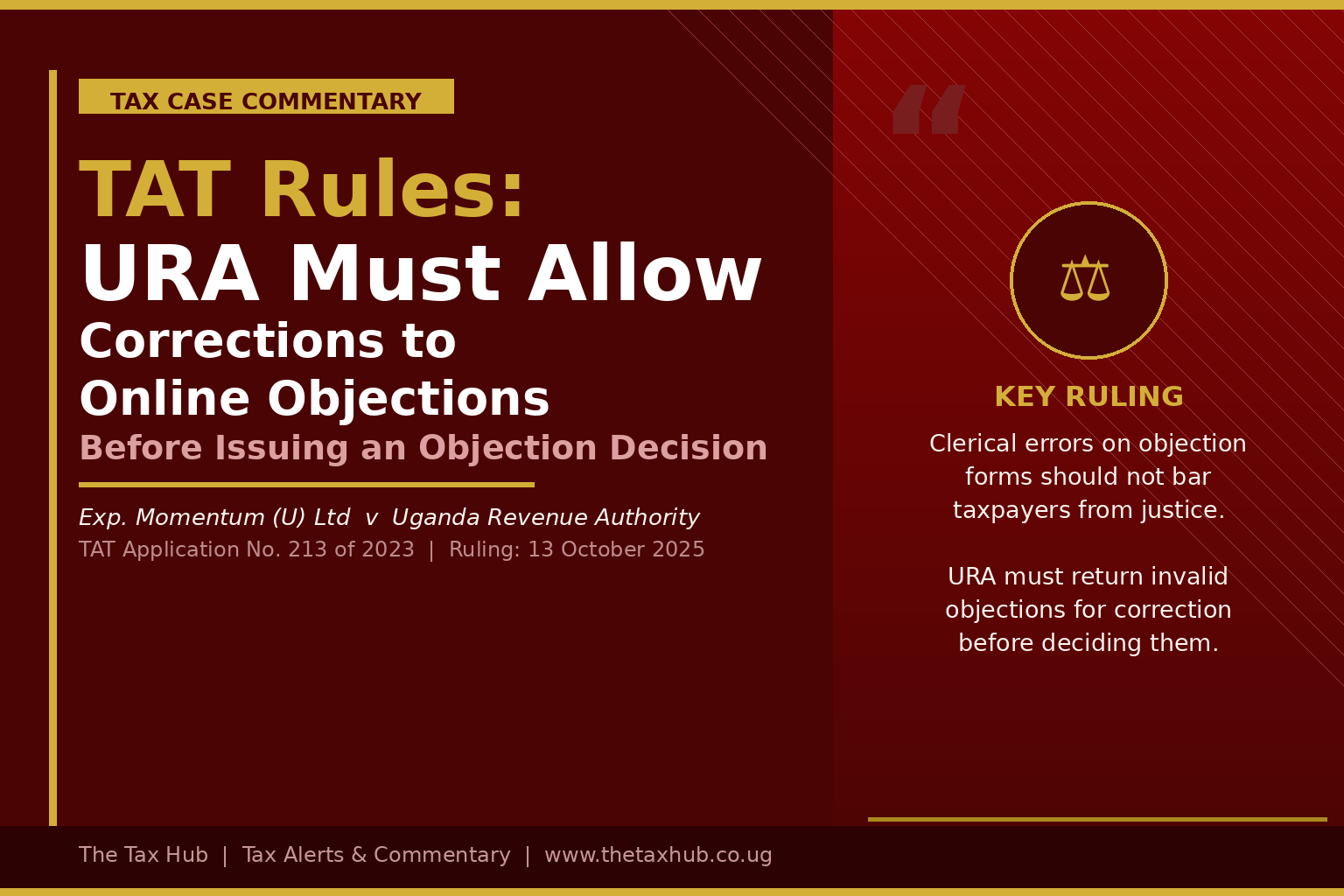

When a Clerical Error Almost Cost a Taxpayer Everything

Exp. Momentum (U) Ltd v Uganda Revenue Authority

TAT Application No. 213 of 2023 | Ruling: 13th October 2025

A marketing and advertising company did everything right. It kept proper books. It reconciled its VAT and income tax returns. It gathered documents, wrote explanatory notes, and submitted them to URA. And yet, because of a single tick in the wrong column on an online form, it nearly lost the right to have its objection heard at all.

That is the central lesson of Exp. Momentum (U) Ltd v Uganda Revenue Authority, a ruling handed down by the Tax Appeals Tribunal in October 2025. The case raises important questions about procedural fairness, the design of URA’s objections system, and the obligations that both taxpayers and URA carry when an objection is filed.

The Facts

Exp. Momentum (U) Ltd is a company in the marketing and advertising industry. Following a returns examination, URA issued an additional income tax assessment of UGX 263,850,113 on the basis that there were variances between the company’s VAT returns, and its income tax returns specifically, that the VAT returns showed higher sales than the income tax return for the period January to December 2020.

The company objected. Its position was that the variance arose from timing differences in revenue recognition: income that had been accrued in 2019 for jobs executed that year was only invoiced in 2020, meaning it showed up in the 2020 VAT returns but had already been declared and taxed in the 2019 income tax return. No income was hidden. The numbers simply followed different recognition rules across the two tax regimes.

The company provided URA with supporting documentation management accounts, bank statements, reconciliations, and detailed explanatory writeups. It also requested a meeting to walk URA through the information. That meeting was never granted.

Arguments

The Company

The company argued that a clerical error on the objection form should not strip a taxpayer of its right to access justice. The grounds of objection set out in Section C of the same form clearly articulated a dispute with the assessment. The documents it submitted showed, beyond doubt, that it was challenging the assessment, not accepting it.

On the merits, it submitted that the variance between its VAT and income tax returns did not represent undeclared income. It arose from the legitimate difference in income recognition between the two tax regimes: income tax follows accrual accounting under IAS 18, while VAT is triggered at the point of invoicing or delivery under the VAT Act. A portion of the variance also arose from technical fees paid to a foreign service provider, which were incorrectly captured under output VAT in the monthly returns but were not the company’s income.

URA

URA maintained that the objection form unambiguously reflected a non-disputed amount. Its Objections Officer confirmed that the system showed the figure as non-disputed, and this was not contradicted at the time. URA’s position was clear: where a taxpayer does not dispute an assessed amount and URA accordingly maintains it, the taxpayer cannot later claim it intended to dispute the same. The attempt to revisit the matter in May 2022 was an afterthought, made after the objection decision had already been issued.

On the further additional assessment of UGX 33,554,049, URA submitted it was lawfully raised: the company had double-claimed a rent expense, and when it corrected this error through an amended objection return, the chargeable income increased generating the additional tax.

The Tribunal’s Ruling

The Tribunal examined the objection form carefully. It found something important: while the form’s columns showed the amount as non-disputed, Section C of the same form which sets out the grounds of objection clearly showed that the company was disputing the assessment. The email attaching the requested supporting documents also demonstrated that the company was challenging URA’s position, not accepting it.

The Tribunal held that URA’s online objection system has a built-in mechanism for exactly this situation. When a Valid Objection Notice is filed, URA is required to assess its validity before proceeding to determine it on the merits. Sections B and C of the Valid Objection Notice provide a pathway for invalid objections to be returned to the taxpayer and corrected. URA ought to have used this mechanism flagging the contradiction, returning the form, and giving the company an opportunity to file a valid objection.

Instead, URA proceeded to issue an objection decision based on an invalid objection. The Tribunal ruled that an objection decision founded on an invalid objection is itself invalid. The assessment of UGX 263,850,113 was remitted back to URA for proper consideration of the variance question specifically, whether the difference between the company’s VAT and income tax returns arose from the accrual of income, as the company had explained.

On the additional assessment of UGX 33,554,049, the Tribunal upheld it. The company’s own correction of a double-claimed expense legitimately increased chargeable income, and the resulting tax was properly assessed.

On the VAT penal tax of UGX 13,327,296, the Tribunal found in the company’s favour. The penalty had been outstanding since 2016. Section 46 of the Tax Procedures Code Act waives any interest and penalty outstanding as at 30 June 2020. The waiver applied, and URA had no basis to maintain the penalty.

My View

This case is a reminder that tax disputes are decided on two tracks simultaneously: the substantive merits, and the procedural framework. A taxpayer can have an entirely correct position on the law and the facts, and still lose or be significantly delayed because of a procedural misstep.

The Tribunal’s ruling that URA should have returned the invalid objection for correction rather than exploiting it is the right outcome. But it took four years of litigation to establish that. The practical lesson is this: treat the objection form with the same rigour you would apply to a court pleading. It is not an administrative formality. It is the foundation of your legal rights in the dispute.

If you have questions about managing tax assessments, the objection process, or reconciling VAT and income tax positions, we are here to help.

This commentary is prepared for informational purposes only and does not constitute legal or tax advice.

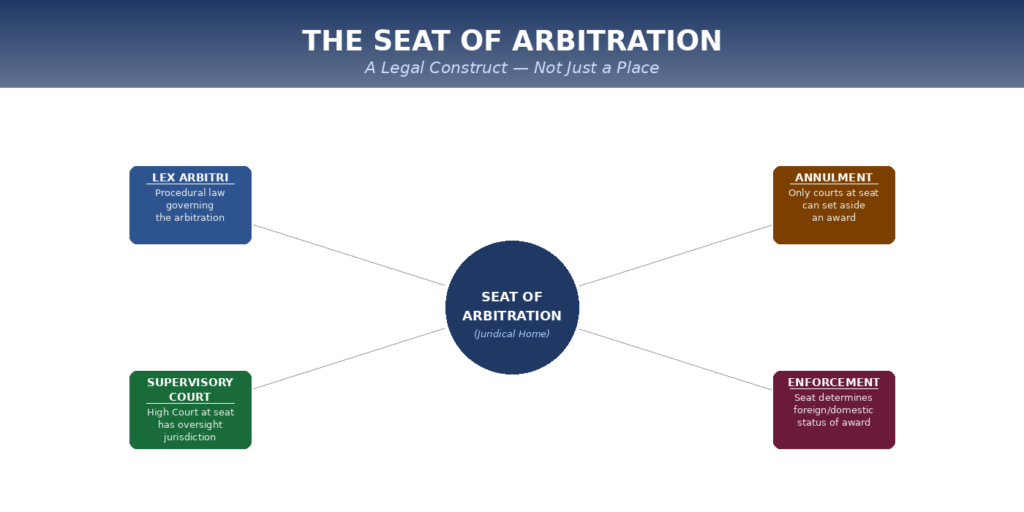

Arbitration has emerged as the preferred mechanism for resolving commercial and investment disputes across the globe. At its heart lies a concept that is both deceptively simple and legally profound the seat of arbitration. The seat is not merely a pin on a map. It is the juridical home of the arbitration: a legal construct that determines the procedural law governing the proceedings, the court with supervisory jurisdiction, and the framework within which any award may be challenged or enforced.

As the volume of commercial activity in Uganda continues to grow, and as the country positions itself as an investment destination within the East African Community and beyond, a clear understanding of the seat of arbitration and of how Uganda’s law treats it is increasingly indispensable for practitioners, businesses, and policymakers alike. This article examines the concept of the seat of arbitration, its legal significance, the statutory framework under the Arbitration and Conciliation Act, Cap. 4 (hereinafter the “Act”), and Uganda’s prospects and challenges as an arbitral seat.

What is the Seat of Arbitration?

The seat of arbitration, also referred to as the “place” of arbitration, is a legal concept that identifies the jurisdiction in which an arbitration is considered to occur. As has been aptly observed, the seat is “a legal construct, not a geographical location.” It does not necessarily refer to the physical location where parties and arbitrators convene hearings may take place in Kampala, Nairobi, Singapore, or entirely over video conferencing yet the seat, and therefore the governing procedural framework, remains wherever the parties have designated.

The seat is best understood as the juridical domicile of the arbitration. It determines which country’s procedural laws, known as the lex arbitri, apply to the proceedings. These laws govern critical matters such as the appointment and challenge of arbitrators, the conduct of proceedings, the availability of interim measures, and most significantly the grounds upon which an award may be set aside.

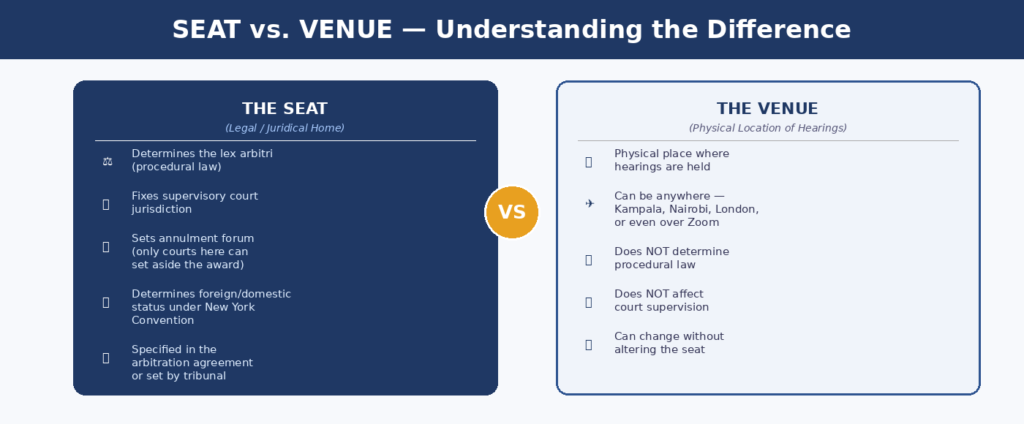

The Distinction Between Seat and Venue

A common source of confusion in practice is the conflation of the seat of arbitration with the venue the physical location where hearings are held. These are distinct legal concepts. The seat establishes the legal framework and determines which courts have supervisory jurisdiction over the arbitration. The venue, on the other hand, is purely a matter of practical convenience and has no legal consequences in itself.

This distinction is preserved under Uganda’s Act, and its practical implications are significant. Parties to an arbitration seated in Kampala may, for reasons of convenience, choose to hold their hearings in Nairobi or London. The physical location of those hearings does not alter the fact that Ugandan law governs the procedure, that Ugandan courts supervise the arbitration, and that any challenge to the award must be brought before the Ugandan courts.

The Statutory Framework: Sections 19 and 20 of the Act

The Arbitration and Conciliation Act, Cap. 4, which commenced on 19 May 2000, is Uganda’s principal statute governing both domestic and international arbitration. Modelled on the UNCITRAL Model Law on International Commercial Arbitration, the Act provides a framework that reflects internationally recognised principles while catering to Uganda’s specific legal context. Sections 19 and 20 of the Act are particularly central to the concept of the seat of arbitration.

Section 19 — Determination of Rules of Procedure

Section 19 of the Act establishes the procedural architecture of arbitral proceedings and embodies the foundational principle of party autonomy. Under subsection (1), the parties are free to agree on the procedure to be followed by the arbitral tribunal. This freedom is broad: parties may adopt the rules of an arbitral institution, craft their own bespoke procedure, or incorporate rules by reference in their arbitration agreement.

Where the parties have made no such agreement, subsection (2) grants the tribunal wide discretion to conduct the arbitration in whatever manner it considers appropriate. This discretion expressly extends, under subsection (3), to matters of evidence the tribunal may determine the admissibility, relevance, materiality, and weight of any evidence placed before it. Unlike litigation, arbitration under the Act is therefore not bound by the formal rules of evidence applicable in court proceedings.

Subsection (4) introduces an important procedural protection: every witness giving evidence and every person appearing before an arbitral tribunal enjoys at least the same privileges and immunities as witnesses and advocates in proceedings before a court. This provision ensures that the arbitral process commands a level of procedural integrity and dignity comparable to that of the formal court system, while preserving its distinctive flexibility.

Section 20 — Place of Arbitration

Section 20 is the provision most directly concerned with the seat. Under subsection (1), the parties are free to agree on the place of arbitration. This choice carries profound legal consequences it determines the lex arbitri, defines the supervisory court, and sets the stage for any annulment proceedings.

Where the parties fail to agree on the place, subsection (2) empowers the arbitral tribunal to make that determination. The tribunal’s discretion must be exercised having regard to the costs involved, the circumstances of the case, and the convenience of the parties a balanced approach ensuring that the seat is not imposed in a manner that prejudices either party.

Subsection (3) preserves the important distinction between seat and venue by providing that, notwithstanding the agreed or determined place of arbitration, the tribunal may meet at any location it considers appropriate for consultations, hearings, or inspection of documents, goods, or property. The legal seat therefore remains fixed, while the physical conduct of proceedings retains the flexibility that is one of arbitration’s most valued features.

Why the Seat of Arbitration Matters

The choice of seat carries far-reaching legal and practical implications. Understanding these consequences is essential both for parties entering arbitration agreements and for those already involved in proceedings.

A. Governing Procedural Law (Lex Arbitri)

The most immediate legal impact of the seat is the determination of the lex arbitri the procedural law governing the arbitration. This includes the rules applicable to the appointment and challenge of arbitrators, the availability of interim relief, the conduct of proceedings, obligations of confidentiality, and the extent to which courts may intervene in the arbitral process. A seat in Uganda therefore subjects the arbitration to the procedural regime of the Act, including its UNCITRAL-based framework.

B. Court Supervision and Supervisory Jurisdiction

Courts at the seat of arbitration exercise supervisory jurisdiction over the proceedings. In Uganda, this supervisory role is vested in the Commercial Division of the High Court. Under this jurisdiction, the court may appoint arbitrators where the parties cannot agree, decide on challenges to the appointment or conduct of arbitrators, grant interim measures in support of arbitration, and most critically entertain applications to set aside an arbitral award.

Under Article I(1) of the 1958 New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards, the determination of whether an award is a “foreign award” depends on the seat. Courts at the seat are therefore the “home court” of the arbitration, while courts elsewhere are treated as foreign courts with considerably more limited supervisory powers.

C. Annulment Proceedings and Enforcement Risk

Perhaps the most consequential implication of the seat relates to annulment. Only the courts at the seat have jurisdiction to set aside an arbitral award. This principle has been affirmed by Uganda’s High Court in cases such as Aya Investments (U) Limited v Industrial Development Corporation of South Africa Ltd, where the court held that an arbitral award can only be set aside at the seat of arbitration.

If an award is set aside at the seat, enforcement in other jurisdictions may be refused under Article V(1)(e) of the New York Convention. While some jurisdictions, most notably France, may in narrow circumstances enforce awards that have been annulled at the seat, this remains the exception. In practice, an annulment at the seat can be fatal to enforcement efforts globally. The choice of a pro-arbitration seat is therefore a critical risk management decision.

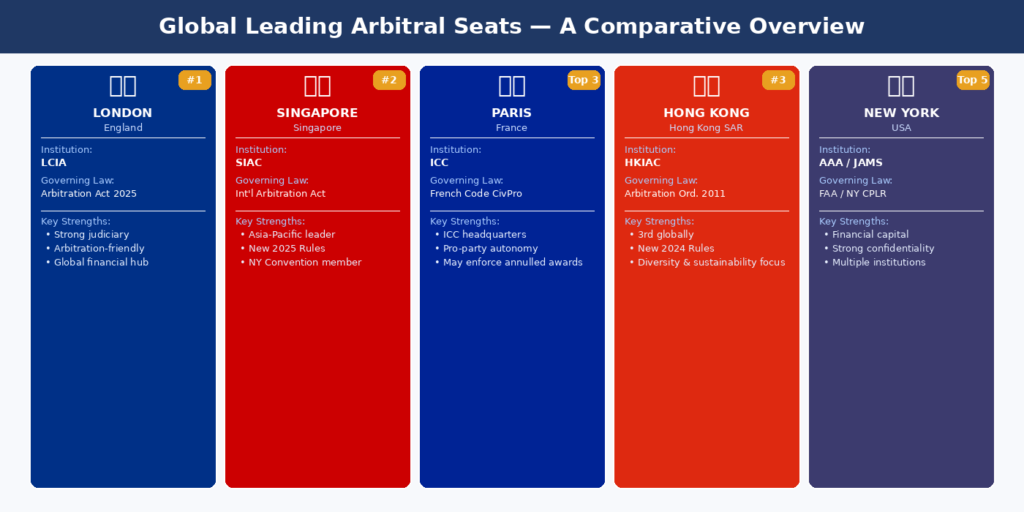

Uganda as a Seat of Arbitration

A. The Legal Framework

Uganda’s arbitration framework is, by design, conducive to effective arbitration. The Act, modelled on the UNCITRAL Model Law, enshrines party autonomy as a central organising principle. Ugandan courts have, in recent years, consistently affirmed their commitment to the principle of minimal judicial interference in arbitration. There is, in general, no right of appeal against a High Court decision on an application to set aside an arbitral award, except where the parties have agreed otherwise or where leave is granted.

Uganda is also a signatory to both the New York Convention and the ICSID Convention, both of which are domesticated by the Act. This membership means that foreign arbitral awards are readily enforceable in Uganda and that awards made in Uganda are enforceable in the over 170 signatory states to the New York Convention. The Act further provides that an award shall be treated as made at the seat of the arbitration regardless of where it was signed, dispatched, or delivered — a provision that reinforces the legal primacy of the seat.

B. Arbitral Institutions in Uganda

The institutional landscape for arbitration in Uganda has grown meaningfully in recent years. The chartered institution of Arbitrators- Uganda chapter plays a big role in training and education of Uganda professions. The International Centre for Arbitration and Mediation in Kampala (ICAMEK), established in 2018 and officially recognised as an appointing authority under the Act by the Minister of Justice in 2020 through Legal Notice No. 4 of 2020, has attracted both domestic and international parties and maintains a panel with an increasing number of foreign international arbitrators. Its 2018 Arbitration Rules include provisions for the consolidation of separate proceedings and reflect standards comparable to other established regional centres. The Centre for Alternative Dispute Resolution (CADER) also continues to play a role in domestic dispute resolution.

C. Challenges and the Path Forward

Despite these foundations, Uganda faces genuine challenges in establishing itself as a preferred international seat. International arbitrations involving Ugandan parties have often been conducted under the auspices of ICSID or the ICC, with seats designated outside the country. The Uganda Law Reform Commission has acknowledged these limitations and has conducted a comprehensive review of the Act, culminating in the preparation of a draft amending Bill. The recommended reforms aim to address gaps in the existing framework, align Uganda’s legislation more closely with evolving international best practices, and enhance the clarity and effectiveness of the arbitration regime.

Criteria for Choosing a Seat

When selecting a seat of arbitration, parties and their counsel should weigh the following interconnected factors:

The seat should have a modern arbitration law, ideally modelled on the UNCITRAL Model Law, that ensures the effective enforcement of awards.

The local courts at the seat should be supportive of arbitration and refrain from undue interference in the arbitral process.

The scope for appeals or challenges to awards on questions of law or substance should be limited, preserving the finality of the award.

Recourse against awards should be available only in accordance with the spirit and provisions of the New York Convention narrow, internationally recognised, and predictable.

The seat should ideally have an established track record, giving parties confidence that the legal framework has been tested.

Practical considerations including cost, accessibility, and the availability of qualified arbitrators and legal counsel should also inform the decision.

Applying these criteria to Uganda, the legal framework is sound and the judicial posture increasingly favourable. The remaining gap lies primarily in track record and institutional reputation factors built incrementally through consistent performance over time.

Conclusion

The seat of arbitration is not a technicality it is the legal home of your dispute. Get it right, and you have a clear procedural framework, a supportive court, and an enforceable award. Get it wrong, and the consequences can unravel everything.

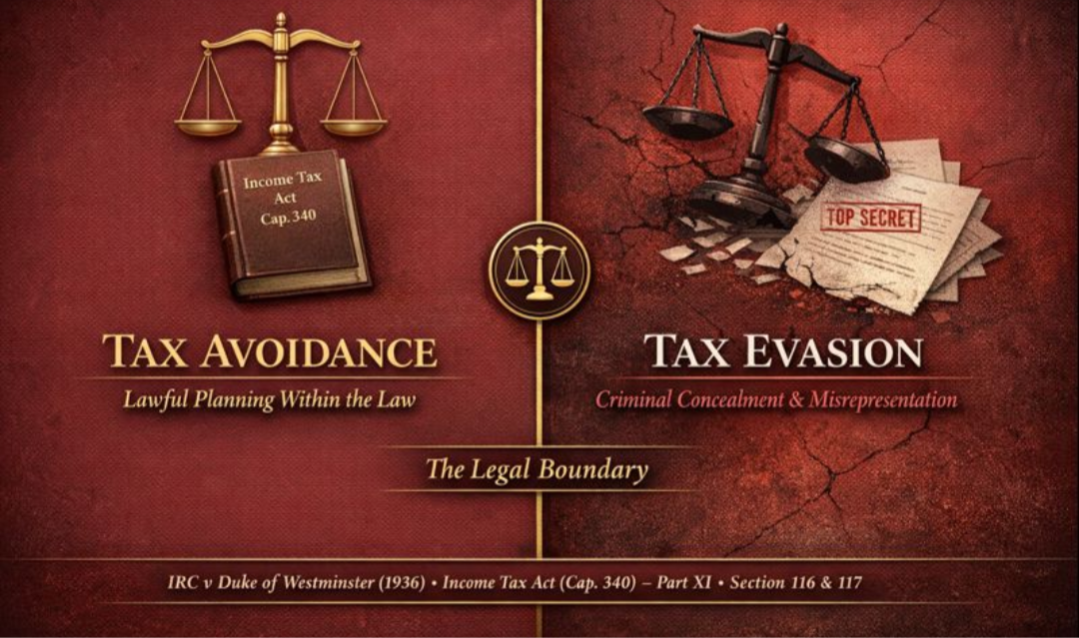

The distinction between tax avoidance and tax evasion is one of the most significant concepts in revenue law. While both practices result in a reduction of the tax payable to the state, they differ fundamentally in their legal character: one is permissible, the other is a criminal offence.

This paper examines both concepts within the Ugandan legal framework, drawing on judicial authority, academic commentary, and the Income Tax Act (Cap. 340).

Definitions

Academic Authority on Tax Avoidance

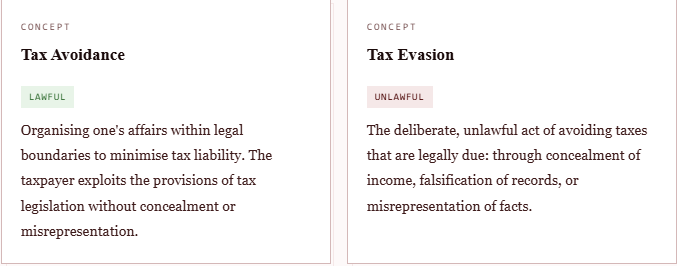

Geoffrey Moses and Sandra Eden, in Principles of Tax Law, define tax avoidance as the act of organising one’s affairs within legal boundaries in order to reduce the tax bill, an approach that is considered entirely lawful. The taxpayer does not conceal any facts or misrepresent any transaction; rather, they exploit the provisions of the tax legislation to their advantage.

Academic Authority on Tax Evasion

Professor Bakibinga, in Revenue Law in Uganda (2nd ed, p. 205), defines tax evasion as the unlawful act of evading taxes. Unlike avoidance, evasion exposes the taxpayer to criminal liability and potential prosecution by the Uganda Revenue Authority.

The Judicial Foundation: The Westminster Principle

IRC v Duke of Westminster [1936] AC 1 · [1935] All ER Rep 501

The Duke replaced his gardeners’ wages with periodic payments made under a deed of covenant, an arrangement that allowed him to claim a tax deduction and significantly reduce his liability. The House of Lords held the arrangement to be lawful.

Lord Tomlin affirmed the right of every individual to arrange their affairs in such a manner as to attract less tax, provided those arrangements conform to the law. His Lordship emphasised that courts are bound by the literal meaning of tax legislation and cannot impute a tax liability that the statute does not impose.

This became known as the Westminster Principle, a cornerstone of tax avoidance doctrine in common law jurisdictions, including Uganda. It privileges the legal form of a transaction over any inquiry into the taxpayer’s underlying motive.

Uganda’s Anti-Avoidance Framework

Recognising that the Westminster Principle could be abused, the Ugandan legislature incorporated anti-avoidance measures into Part XI of the Income Tax Act (Cap. 340). Two provisions are of particular significance.

Section 116: Transactions Between Associates

Section 116 empowers the Commissioner General to distribute, apportion, or allocate income, deductions, or credits between associated taxpayers where a transaction does not reflect an arm’s length dealing. The Commissioner may also adjust income from the transfer or licensing of intangible property between associates to ensure it is commensurate with its true economic value. This provision targets arrangements where related parties manipulate transactions to shift income or inflate deductions.

Section 117: Re-characterisation of Transactions

Income Tax Act (Cap. 340) · Section 117(2)

A “tax avoidance scheme” includes any transaction, one of the main purposes of which is the avoidance or reduction of liability to tax.

Section 117 grants the Commissioner General broad discretionary power to re-characterise transactions that form part of a tax avoidance scheme. Specifically, the Commissioner may:

Re-characterise a transaction whose form does not reflect its substance; disregard a transaction that lacks substantial economic effect; or re-characterise any element of a scheme entered into with the purpose of avoiding or reducing tax liability.

This provision introduces a substance-over-form approach, a significant departure from the strict literalism endorsed in the Westminster case, and reflects the legislature’s intent to close gaps that purely form-driven analysis might leave open.

Judicial Application: WB v Commissioner of Income Tax

WB v Commissioner of Income Tax 2 EATC 32

The court considered whether an arrangement involving the transfer of shares to the taxpayer’s children, funded by loans purportedly made by the parents and repayable from dividend income, constituted a genuine commercial transaction or a tax avoidance scheme.

The court held that the transfers of shares to the appellant’s children were genuine commercial transactions. The arrangement was not a sham devised to evade tax, and the transactions carried sufficient economic substance to withstand scrutiny under the applicable provisions of the Act.

This case illustrates the courts’ willingness to look beyond the form of a transaction to assess its true commercial substance, an approach now codified in section 117 of the Income Tax Act, while also demonstrating that transactions with genuine economic effect will be respected even where they produce a tax benefit.

Conclusion

The line between lawful tax avoidance and unlawful tax evasion is a critical one in Ugandan revenue law. While the common law tradition recognises the taxpayer’s right to minimise their tax burden through legitimate planning, the Income Tax Act has progressively curtailed aggressive avoidance schemes through the anti-avoidance provisions of Part XI.

The substance-over-form doctrine embedded in section 117 ensures that transactions devoid of genuine commercial purpose are not permitted to erode the tax base. Practitioners and taxpayers must therefore carefully navigate this boundary, exercising their lawful planning rights while remaining alert to the Commissioner General’s broad powers of re-characterisation.

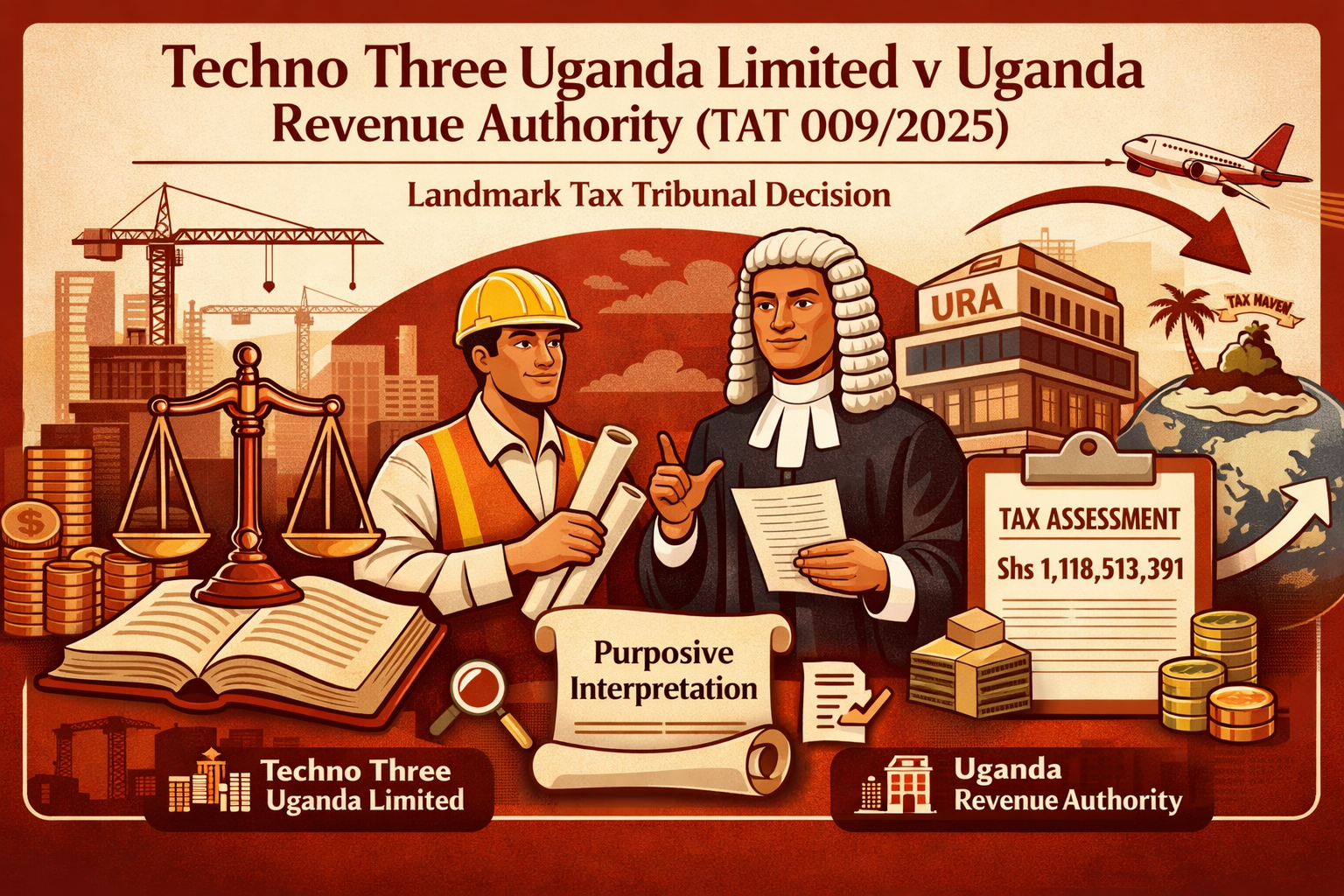

Techno Three Uganda Limited v Uganda Revenue Authority (TAT 009/2025)

Introduction

The Tax Appeals Tribunal’s ruling in Techno Three Uganda Limited v Uganda Revenue Authority (TAT 009/2025), delivered on 4th February 2026, represents a watershed moment in Ugandan tax jurisprudence. This case demonstrates exemplary judicial practice by applying purposive statutory interpretation to prevent absurd outcomes while simultaneously providing evidence-based policy recommendations to government. The Tribunal’s approach extends beyond traditional adjudication to embrace an advisory role that could reshape how anti avoidance provisions are applied in Uganda’s tax system.

Brief Facts

Techno Three Uganda Limited, a construction and civil engineering company, challenged an assessment of Shs. 1,118,513,391 issued by the Uganda Revenue Authority for tax years 2018-2020. The URA alleged that the Applicant had overclaimed interest expenses, arguing that it was part of a “group” with common underlying ownership, thereby restricting its interest deduction to 30% of EBITDA under Section 25(3) of the Income Tax Act.

The factual matrix revealed that the Applicant’s shareholders Jang Bahader Singh Wazir and Amandeep Singh had registered three other companies however, these companies were non-operational entities filing nil income tax returns except of one. Critically, the Applicant’s interest expenses arose from borrowings from unrelated third-party Ugandan banks Bank of Baroda and Bank of Africa not from intercompany loans.

Question for Determination

The central issue before the Tribunal was whether the Applicant was liable to pay the assessed tax arising from the Respondent’s restriction of interest deductions. This seemingly straightforward question concealed complex sub-issues:

Does common shareholding alone constitute a “group” under Section 25(5)(b)?

Should Section 25(3) apply to dormant, non-trading entities?

What was the legislative intent behind this provision?

Does borrowing from third-party domestic lenders trigger the interest restriction designed to combat multinational profit shifting?

The Court’s Reasoning

The Tribunal’s analysis commenced with a fundamental question: does this case warrant departure from literal statutory interpretation in favour of the purposive approach? The answer, grounded in the principle that literal interpretation should yield when it produces absurdity, was affirmative.

Legislative Intent and Historical Context

In a display of rigorous legal research, the Tribunal examined the Hansard records from the 24 May 2018 parliamentary debate on the Income Tax (Amendment) Bill. This revealed that the Legislature’s primary concern was multinational companies “lending amongst themselves” to reduce chargeable income in Uganda. As MP Mwiru stated, the focus was on “multinational companies” engaged in groups that shift profits through interest deductions. The Tribunal traced the provision’s origin to the 2015 OECD Base Erosion and Profit Shifting (BEPS) Report, Action 6, which recommended curbing excessive interest deductions to prevent tax base erosion.

The historical evolution proved instructive. Before 2018, Section 89 (thin capitalization rules) targeted only foreign-controlled resident companies. The 2018 amendment introduced Section 25(3), extending interest restrictions to local enterprises but retaining the anti-avoidance purpose preventing companies from using interest deductions to artificially reduce taxable income.

Substance Over Form Principle

The Tribunal’s application of the Ramsay Principle that tax outcomes should reflect economic reality rather than mere legal documentation proved decisive. The central finding at paragraph 61-62 established that applying Section 25(3) to groups comprised of dormant, non-trading entities existing only on paper would be unjustified. As the Tribunal stated, the “substance over form principle” ensures “that tax burdens are fair and do not unnecessarily hinder economic growth or encourage artificial, non-productive behaviour.”

The factual analysis revealed the absurdity of the URA’s position. Satech Industries was incorporated after the assessment period and later struck off. The other companies had no business operations, significant assets, or employees. They filed nil returns, indicating no economic activity whatsoever. The interest in question arose from borrowings from unrelated Ugandan banks whose interest income would be taxed in Uganda presenting no base erosion risk that Section 25(3) was designed to prevent.

Tax Cohesion and Policy Context

The Tribunal distinguished between multinational profit shifting and domestic lending. When a multinational group lends internally, interest deductions in Uganda correspond to untaxed income abroad, eroding Uganda’s tax base. However, when a Ugandan company borrows from domestic banks, the interest deduction is matched by taxable interest income in the same jurisdiction maintaining tax cohesion and generating government revenue.

To support its analysis, the Tribunal referenced Uganda’s national development frameworks. Vision 2040 identifies poor access to finance as a major constraint, with Uganda ranking 112th out of 183 countries. The National Development Plan IV notes that interest rates averaged 19.1% over five years against a Central Bank rate of 8.4%, making business expensive for the private sector. The Tenfold Growth Strategy targets growing private sector credit from 11% of GDP (2023) to 100% by 2040. Restricting interest deductions for legitimate domestic borrowing directly contradicts this objective.

The Tribunal also identified perverse incentives created by literal application. A business owner structuring operations into separate companies for legitimate reasons would be denied full interest deductions, while consolidating everything into one company would preserve the deduction allowing form to prevail over economic substance.

Final Determination

The Tribunal ruled that the assessment of Shs. 312,539,675 was untenable and set it aside, awarding costs to the Applicant. The legal principle established requires that “group” status under Section 25(5)(b) demands more than common ownership it requires economic substance, active business operations, and actual economic relationships between members. The provision does not apply to dormant entities, companies incorporated after the assessment period, or borrowing from unrelated third-party domestic lenders.

Recommendations to Government

Crucially, the Tribunal recommended that the Ministry of Finance revisit Section 25(3) and (5), focusing on their intended purpose and alignment with broader economic goals. The specific proposal was to restrict the provision to multinational enterprises, as its core purpose is preventing base erosion and profit shifting by such enterprises. This recommendation aligns with original legislative intent, international best practices under the OECD BEPS framework, Uganda’s development objectives, and principles of tax cohesion.

Conclusion

This ruling’s significance extends far beyond the immediate case, impacting tax interpretation, administration, and policy development in several profound ways. The case establishes a new standard for interpreting anti-avoidance provisions. It demonstrates that purposive interpretation must consider legislative history, international context, and broader policy objectives. The Tribunal showed that mechanical application of tax rules, ignoring economic substance, produces unjust outcomes contrary to legislative intent. This precedent will guide interpretation of similar provisions, requiring tax authorities to examine the substance of transactions rather than merely their legal form.

Perhaps most groundbreaking is the Tribunal’s extension of its role beyond passive adjudication to active policy engagement. Traditional judicial restraint might have stopped at ruling the provision inapplicable to this case. Instead, the Tribunal provided evidence-based analysis using economic data, national development plans, international standards, and parliamentary debates to identify systemic problems and recommend solutions. This represents judicial activism in its best form respecting legislative supremacy while contributing specialized expertise to inform policy reform.