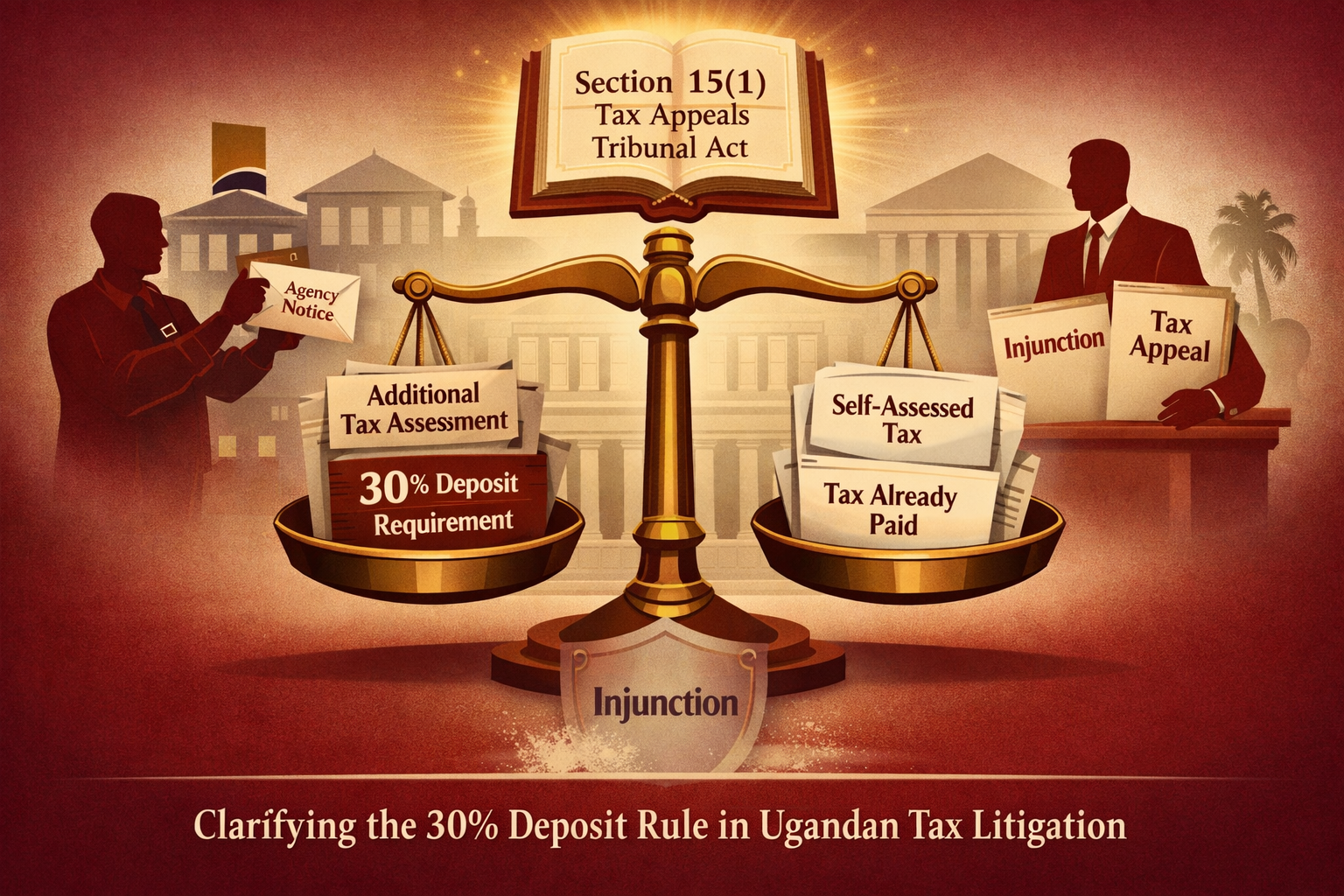

Brief facts

In 2022, the appellant made and paid self-assessments for Local Excise Duty and Value Added Tax. Following an audit, the 1st respondent issued additional administrative assessments for both taxes, which the appellant disputed. While the appellant paid the amounts it had self-assessed, it applied to the Tax Appeals Tribunal for review of the additional assessments and sought a temporary injunction restraining their collection. On 7 March 2022, the Tribunal granted the injunction on condition that the appellant pay 30% of the tax in dispute or the tax not in dispute, whichever was greater. A dispute arose when the 1st respondent demanded payment of 30% of the disputed tax, while the appellant maintained that the amount already paid as tax not in dispute exceeded that threshold. In an attempt to recover the amount, the 1st respondent issued third-party agency notices to the 2nd and 3rd respondents on 19 April 2022, which they declined to honour. Consequently, on 29 April 2022, the 1st respondent filed an application seeking to have the appellant and the 2nd and 3rd respondents sanctioned for contempt of the Tribunal’s conditional injunction order.

Question for determination

Whether the condition imposed by the Tax Appeals Tribunal requiring payment of “30% of the tax in dispute or the tax not in dispute, whichever is greater” was satisfied by the taxpayer’s prior payment of the self-assessed tax, or whether the 30% deposit applied strictly to the disputed additional assessment raised by URA.

Court’s Reasoning and Final Determination

The Court reasoned that section 15(1) of the Tax Appeals Tribunals Act is a clear and self contained provision whose interpretation must be confined to its express wording. In applying settled principles of statutory interpretation particularly the strict and literal approach applicable to taxing statutes the Court held that the phrase “tax assessed” refers solely to the disputed additional assessment raised by the Uganda Revenue Authority, and not to tax previously self-assessed and paid by the taxpayer. The Court rejected any attempt to import concepts from the Tax Procedures Code Act or to rely on equitable considerations, emphasizing that tax obligations can only arise from clear statutory language and cannot be extended by implication.

On jurisdiction and procedure, the Court found that the Tax Appeals Tribunal exceeded its mandate by invoking contempt proceedings to enforce compliance with a conditional injunction. It reasoned that the Tribunal’s order was self-executing, such that failure to comply with the 30% payment condition automatically resulted in the lapse of the injunction without the need for punitive enforcement. Consequently, the Tribunal lacked jurisdiction to punish the appellant for contempt. The Court further dismissed URA’s objection to the appeal, holding that appellate rights extend to ancillary and interlocutory matters, including contempt findings, to prevent denial of access to justice.

Final Determination

Accordingly, the High Court allowed the appeal, set aside the Tribunal’s finding of contempt and the fines imposed, and affirmed that the only legal consequence of non-compliance with the 30% deposit condition is the automatic lapse of the injunction. In doing so, the Court reinforced certainty in the application of the 30% deposit rule, delineated the limits of the Tribunal’s jurisdiction, and upheld the rule of law in the resolution of tax disputes.

Conclusion

In Nile Breweries Limited v Uganda Revenue Authority & Others (Civil Appeal No. 14 of 2022), the Court clarified that the 30% deposit rule applies only to the disputed additional tax assessment, not to prior self assessed payments. It held that the Tax Appeals Tribunal acted beyond its jurisdictionby treating non-compliance with the 30% condition as contempt. The proper consequence of non-payment is the automatic lapse of the injunction, not sanctions. The Court also affirmed that appeals against ancillary matters, including contempt, are competent, thereby protecting taxpayers’ rights and ensuring certainty and legality in tax dispute resolution.

Leave a Reply