Introduction

The distinction between tax avoidance and tax evasion is one of the most significant concepts in revenue law. While both practices result in a reduction of the tax payable to the state, they differ fundamentally in their legal character: one is permissible, the other is a criminal offence.

This paper examines both concepts within the Ugandan legal framework, drawing on judicial authority, academic commentary, and the Income Tax Act (Cap. 340).

Definitions

Academic Authority on Tax Avoidance

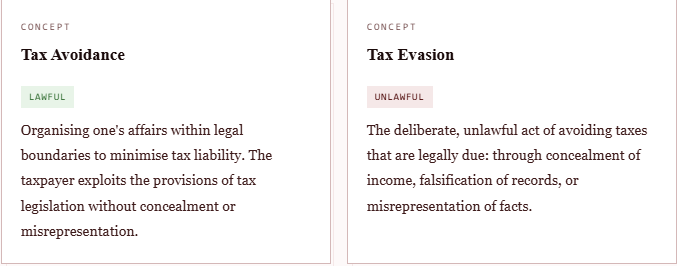

Geoffrey Moses and Sandra Eden, in Principles of Tax Law, define tax avoidance as the act of organising one’s affairs within legal boundaries in order to reduce the tax bill, an approach that is considered entirely lawful. The taxpayer does not conceal any facts or misrepresent any transaction; rather, they exploit the provisions of the tax legislation to their advantage.

Academic Authority on Tax Evasion

Professor Bakibinga, in Revenue Law in Uganda (2nd ed, p. 205), defines tax evasion as the unlawful act of evading taxes. Unlike avoidance, evasion exposes the taxpayer to criminal liability and potential prosecution by the Uganda Revenue Authority.

The Judicial Foundation: The Westminster Principle

IRC v Duke of Westminster [1936] AC 1 · [1935] All ER Rep 501

The Duke replaced his gardeners’ wages with periodic payments made under a deed of covenant, an arrangement that allowed him to claim a tax deduction and significantly reduce his liability. The House of Lords held the arrangement to be lawful.

Lord Tomlin affirmed the right of every individual to arrange their affairs in such a manner as to attract less tax, provided those arrangements conform to the law. His Lordship emphasised that courts are bound by the literal meaning of tax legislation and cannot impute a tax liability that the statute does not impose.

This became known as the Westminster Principle, a cornerstone of tax avoidance doctrine in common law jurisdictions, including Uganda. It privileges the legal form of a transaction over any inquiry into the taxpayer’s underlying motive.

Uganda’s Anti-Avoidance Framework

Recognising that the Westminster Principle could be abused, the Ugandan legislature incorporated anti-avoidance measures into Part XI of the Income Tax Act (Cap. 340). Two provisions are of particular significance.

Section 116: Transactions Between Associates

Section 116 empowers the Commissioner General to distribute, apportion, or allocate income, deductions, or credits between associated taxpayers where a transaction does not reflect an arm’s length dealing. The Commissioner may also adjust income from the transfer or licensing of intangible property between associates to ensure it is commensurate with its true economic value. This provision targets arrangements where related parties manipulate transactions to shift income or inflate deductions.

Section 117: Re-characterisation of Transactions

Income Tax Act (Cap. 340) · Section 117(2)

A “tax avoidance scheme” includes any transaction, one of the main purposes of which is the avoidance or reduction of liability to tax.

Section 117 grants the Commissioner General broad discretionary power to re-characterise transactions that form part of a tax avoidance scheme. Specifically, the Commissioner may:

Re-characterise a transaction whose form does not reflect its substance; disregard a transaction that lacks substantial economic effect; or re-characterise any element of a scheme entered into with the purpose of avoiding or reducing tax liability.

This provision introduces a substance-over-form approach, a significant departure from the strict literalism endorsed in the Westminster case, and reflects the legislature’s intent to close gaps that purely form-driven analysis might leave open.

Judicial Application: WB v Commissioner of Income Tax

WB v Commissioner of Income Tax 2 EATC 32

The court considered whether an arrangement involving the transfer of shares to the taxpayer’s children, funded by loans purportedly made by the parents and repayable from dividend income, constituted a genuine commercial transaction or a tax avoidance scheme.

The court held that the transfers of shares to the appellant’s children were genuine commercial transactions. The arrangement was not a sham devised to evade tax, and the transactions carried sufficient economic substance to withstand scrutiny under the applicable provisions of the Act.

This case illustrates the courts’ willingness to look beyond the form of a transaction to assess its true commercial substance, an approach now codified in section 117 of the Income Tax Act, while also demonstrating that transactions with genuine economic effect will be respected even where they produce a tax benefit.

Conclusion

The line between lawful tax avoidance and unlawful tax evasion is a critical one in Ugandan revenue law. While the common law tradition recognises the taxpayer’s right to minimise their tax burden through legitimate planning, the Income Tax Act has progressively curtailed aggressive avoidance schemes through the anti-avoidance provisions of Part XI.

The substance-over-form doctrine embedded in section 117 ensures that transactions devoid of genuine commercial purpose are not permitted to erode the tax base. Practitioners and taxpayers must therefore carefully navigate this boundary, exercising their lawful planning rights while remaining alert to the Commissioner General’s broad powers of re-characterisation.

Leave a Reply to Peter Cancel reply